Tax season is approaching fast, and if you're like most small business owners using QuickBooks Online, there's a good chance your books contain costly errors that could create major headaches come April. The hard truth? Even with QuickBooks' user-friendly interface, I've seen countless businesses make the same critical mistakes that not only mess up their financial reports but can also trigger IRS red flags.

Here's what's particularly frustrating: most of these errors are completely preventable. After working with hundreds of small businesses, I've identified the seven most damaging QuickBooks Online mistakes that consistently show up in our client audits. The good news? You can fix every single one of them before tax season hits.

Mistake #1: Skipping Monthly Bank Reconciliations

The Problem: Many business owners assume QuickBooks' bank feed eliminates the need for reconciliation. This couldn't be more wrong. Without regular reconciliation, errors, duplicates, and missing transactions accumulate for months without detection, creating a snowball effect that becomes nearly impossible to untangle.

The Reality Check: Your QuickBooks balance might show $15,000 while your actual bank account has $12,500. That $2,500 difference? It could be duplicate transactions, missed bank fees, or incorrectly categorized transfers that will surface during tax preparation.

The Fix:

Reconcile every bank and credit card account monthly, without exception

Treat reconciliation like balancing a checkbook: match every transaction

Set a recurring calendar reminder for the same date each month

If you find discrepancies, investigate immediately rather than forcing the reconciliation

Pro Tip: A properly reconciled account in QuickBooks will have a small checkmark next to the account balance. No checkmark means you're flying blind.

Mistake #2: Creating Duplicate Income and Expenses

The Problem: This is perhaps the most serious error I encounter. Duplicate transactions commonly occur when business owners create invoices and receive payments but fail to properly match the bank deposit to the invoice. Instead, they record the deposit as new income, effectively doubling their revenue.

The Cascade Effect: Duplicate income inflates your profit margins, increases your tax liability, and makes financial planning impossible. On the expense side, recording both a bill and its payment creates artificially high costs that skew every business decision.

The Fix:

Always use the "Find Match" feature instead of "Add" when processing bank transactions

When customers pay multiple invoices in one deposit, record it as a single combined payment

Regularly scan your Profit & Loss report for unusually high income or expense categories

Delete duplicates by clicking into the transaction and selecting "More > Delete"

Quick Tip: If your income suddenly jumps 40% in a month without explanation, you likely have duplicate revenue entries.

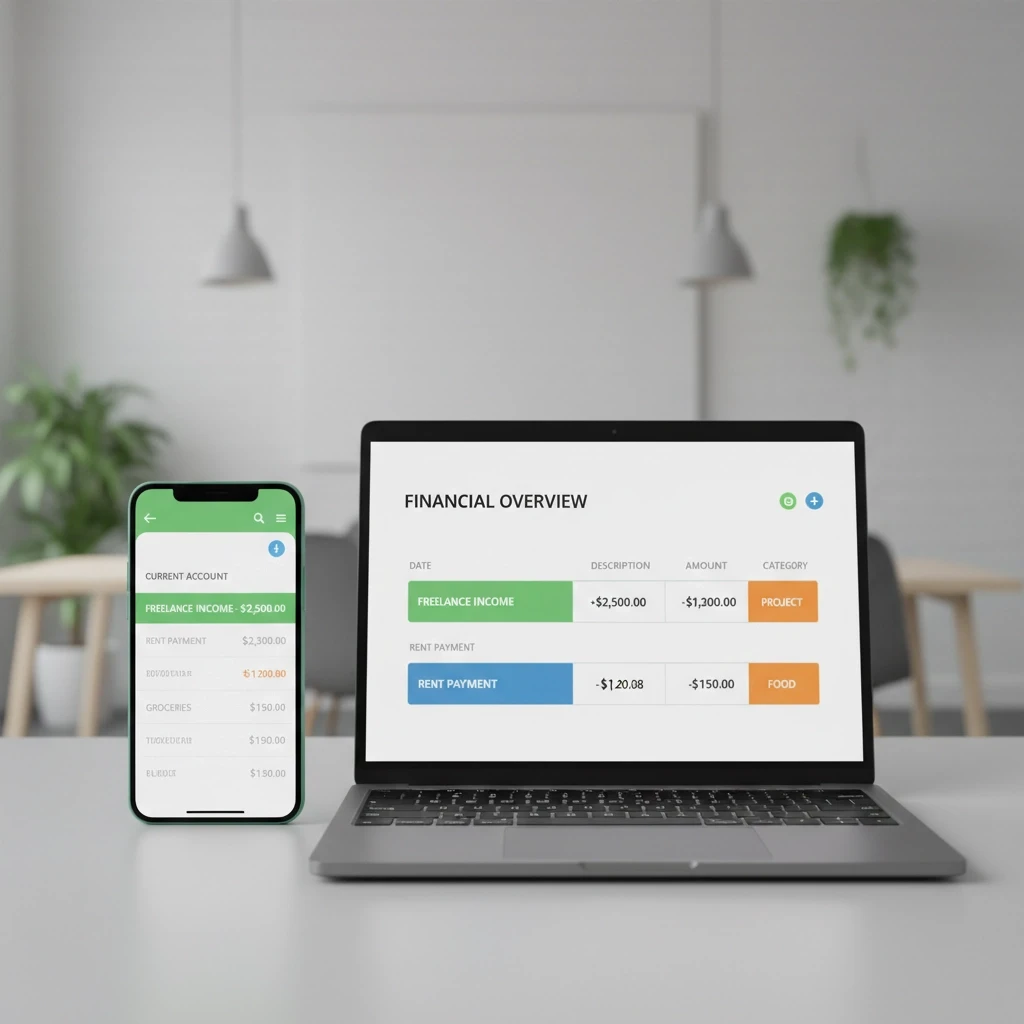

Mistake #3: Misclassifying Transactions and Account Types

The Problem: Incorrect categorization creates wildly inaccurate financial reports and can trigger tax complications. I frequently see businesses that accidentally categorize office supplies as equipment purchases or meal expenses as travel costs, distorting their true spending patterns.

Common Account Type Errors: When creating new accounts, QuickBooks defaults to "Bank" (alphabetically first), and users forget to change it. This means expense categories show up as assets, completely throwing off your balance sheet.

The Fix:

Design a logical Chart of Accounts structure before you start entering data

Use sub-accounts instead of posting everything to parent categories

Review your Profit & Loss report monthly to spot obvious miscategorizations

When in doubt about proper categorization, err on the side of being more specific rather than general

Real-World Example: Don't just use "Office Expenses": break it down into "Office Supplies," "Software Subscriptions," and "Communications" for better tax deduction tracking.

Mistake #4: Improper Bank Account Connections

The Problem: Some businesses delay connecting their financial accounts to QuickBooks, while others connect the wrong accounts entirely. Both approaches create gaps in transaction data that require manual entry: and manual entry means human error.

The Hidden Cost: Without proper bank connections, you're essentially doing double work: managing transactions in your bank's system AND manually entering everything into QuickBooks.

The Fix:

Connect all business bank and credit card accounts directly through QuickBooks' secure banking feature

After initial connection, carefully review and categorize older imported transactions

Set up separate QuickBooks connections for each business account: don't try to manage multiple accounts through one connection

Test the connection monthly to ensure transactions are flowing properly

Mistake #5: Blindly Trusting AI Auto-Categorization

The Problem: QuickBooks' AI features are impressive, but they're not infallible. The system might categorize a restaurant charge as postal services based on merchant name similarities, or classify legitimate business software as personal expenses.

Why This Matters: Auto-categorization errors compound over time. One misclassified vendor can throw off months of similar transactions if you've created automatic rules without review.

The Fix:

Review every transaction in the "For Review" tab before accepting it

Examine all automatic rules under Transactions > Rules: avoid creating "auto-add" rules that bypass human review

Base rules on specific bank text rather than generic descriptions

Spot-check your most frequent vendors monthly to ensure consistent categorization

Warning Sign: If your "Miscellaneous" or "Other Expenses" categories are growing rapidly, your AI categorization needs human intervention.

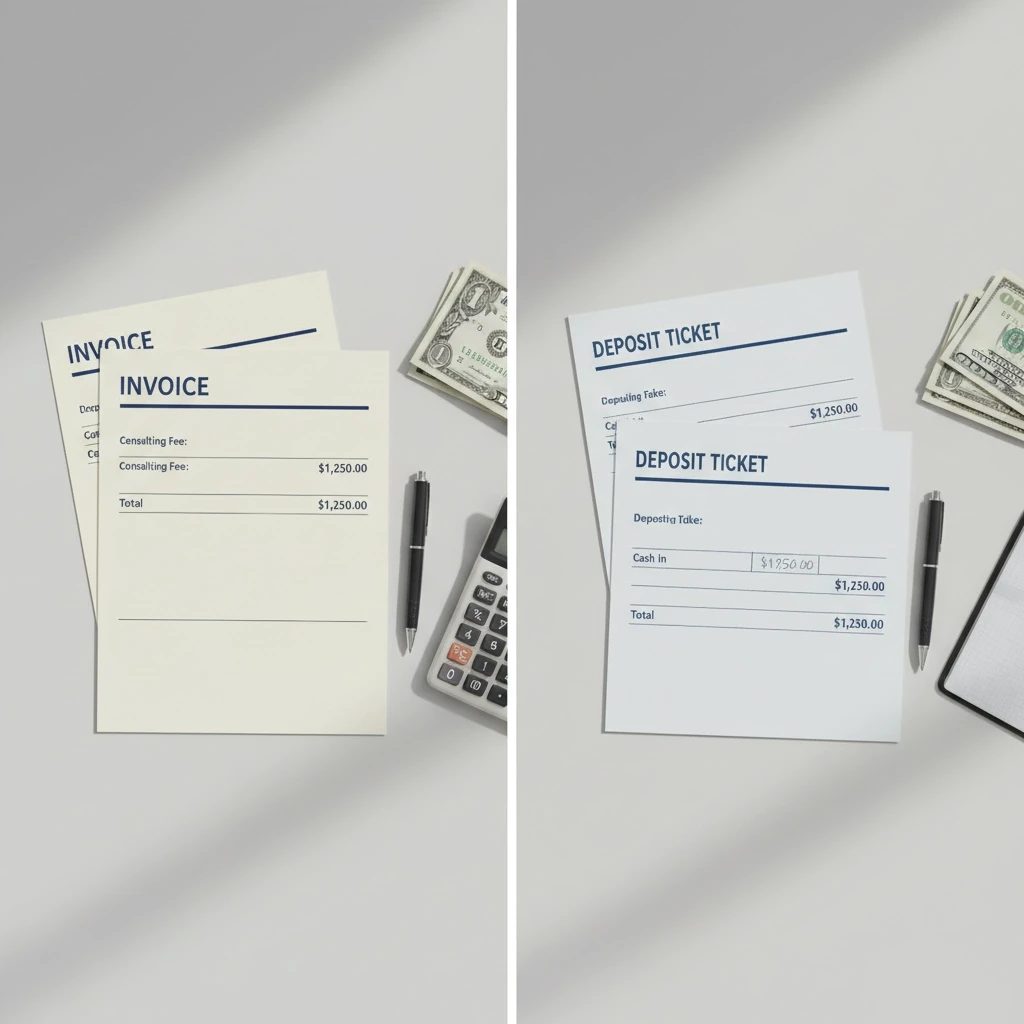

Mistake #6: Failing to Match Deposits to Invoices

The Problem: When you don't properly match bank deposits to customer invoices, several problems cascade: paid invoices still appear on your accounts receivable report, you might accidentally bill clients twice, and your cash flow reports become unreliable.

The Business Impact: You can't effectively manage customer relationships or cash flow when you don't know which invoices have actually been paid.

The Fix:

Use QuickBooks' matching feature to connect every deposit with its corresponding invoice(s)

For customers who pay multiple invoices in one check, record one payment transaction that covers all invoices

Run your Open Invoices report monthly and investigate any invoices older than your standard payment terms

Set up automated payment reminders for truly unpaid invoices, not ones that were already paid but not properly matched

Pro Tip: Your Accounts Receivable aging report should only show genuinely unpaid invoices. If it's full of invoices you know were paid, you have a matching problem.

Mistake #7: Missing Vendor/Customer Assignments and Personal Expense Mixing

The Problem: Transactions without assigned vendor or customer names make it impossible to analyze spending patterns, track vendor relationships, or generate meaningful business intelligence reports. Additionally, mixing personal and business expenses creates tax complications and clouds your true business performance.

The Reporting Challenge: How can you negotiate better rates with vendors if you can't track total annual spending per vendor? How can you identify your best customers without proper transaction assignment?

The Fix:

Assign a vendor or customer name to every transaction in QuickBooks

Maintain strict separation between personal and business expenses by using dedicated business accounts

Create vendor profiles for all regular suppliers, including service providers and contractors

Use the Vendor Detail report monthly to review spending patterns and identify cost-saving opportunities

Getting Tax-Ready: Your Action Plan

Now that you know the seven critical mistakes, here's your immediate action plan:

This Week:

Run a reconciliation on all accounts and fix any discrepancies

Review your Profit & Loss report for obvious categorization errors

Check your Open Invoices report and match any unmatched deposits

This Month:

Audit your Chart of Accounts and consolidate similar categories

Review all automatic rules and remove any that bypass human review

Run vendor and customer reports to ensure all transactions have proper assignments

Before Tax Season:

Complete a final reconciliation of all accounts through December 31st

Generate and review your annual Profit & Loss and Balance Sheet reports

Consider whether your books are clean enough for tax preparation or if you need professional cleanup

The Bottom Line

Clean QuickBooks records aren't just about tax compliance: they're the foundation of smart business decisions. When your books accurately reflect your financial reality, you can confidently pursue growth opportunities, negotiate from positions of strength, and avoid the costly surprises that derail cash flow planning.

If reviewing these seven mistakes reveals serious issues in your QuickBooks setup, don't panic. Most errors can be corrected with systematic cleanup work. However, if you're feeling overwhelmed or discovering problems that go back months, it might be time to bring in professional help to get your books tax-ready.

The investment in clean, accurate bookkeeping always pays dividends when tax season arrives: and your future business decisions depend on having reliable financial data to guide them.

Related Reads for You

Discover more articles that align with your interests and keep exploring.